Category: News

Army Intel Soldier Charged With Selling Secrets About US Weapons, Ops

Army Intel Soldier Charged With Selling Secrets About US Weapons, Ops

An active duty US Army intelligence analyst was arrested on Thursday for sending secret military documents to an unidentified foreign national over a nearly 2-year period. The charges include the unlawful export of defense information to China, but the indictment doesn’t indicate if the foreign national was working for a government.

Sergeant Korbein Schultz was arrested at Fort Campbell, Kentucky, where he’s assigned to the 101st Airborne Division and holds a Top Secret clearance. According to the 25-page indictment, Schultz provided someone identified only as “Conspirator A” — who claimed to reside in Hong Kong — with “information regarding the operability of sensitive U.S. military systems and their capabilities.” Those systems included F-22A fighters, the HH-60W helicopter, intercontinental ballistic missiles, B-52 bombers, air defense systems, HIMARS rocket launchers and hypersonic weapons.

{kind=link}

Schultz, a native of Dallas exurb Wills Point, received 14 payments that totaled some $42,000. It’s not clear if this Sergeant Schultz will plead “I know nothing!”

In addition to weapon-specific information, prosecutors say Schultz also shared big-picture documents, including US research on foreign countries such as China, studies on the future development of US military forces, and recaps of American military drills and operations. The files included documents, maps, manuals and photographs.

Conspirator A’s identity was revealed to the grand jury that indicted him, but, for now, it’s a secret to the rest of us. The indictment only describes the individual as “a foreign national purporting to reside in Hong Kong” who claimed to work for a “geopolitical consulting firm based overseas.” The word “purported” would seem to suggest that investigators either don’t know if Conspirator A lived in Hong Kong, or they know that he or she doesn’t. The indictment doesn’t say if Conspirator A was working for a government.

There’s something of a disconnect between the indictment — which includes multiple charges of Unlawful Export of Defense Articles to China — and the Department of Justice press release, which doesn’t mention the China aspect. However, the Export Control Act charges imply that investigators are confident the recipient was in China.

Schultz allegedly shared information about the US HIMARS platform, among many other weapon systems (Serhii Mykhalchuk/Global Images Ukraine/Getty Images via Newsweek)

{kind=link}

Conspirator A sent a variety of specific requests to Schultz. At the outset of the illicit arrangement, Schultz was requested to share lessons learned from the war in Ukraine, and “with those lessons, what the United States could and should do to help defend Taiwan from an attack,” reads the indictment.

After fulfilling that request in the summer of 2022 and receiving a whopping $200, Schultz is said to have proposed a long-term relationship. Prosecutors say it kept going until his recent arrest. In August 2022, he told Conspirator A that he wished he could be Jason Bourne. Then there’s this amusing anecdote:

On or about May 20, 2023, Conspirator A told KORBEIN SCHULTZ that Conspirator A would like to meet him at a Formula 1 race overseas and make him a “senior partner” with a “big signing bonus.” KORBEIN SCHULTZ responded, “Oh snap!”

“The conduct alleged in today’s indictment represents a grave betrayal of the oath sworn to defend our country,” said FBI Executive Assistant Director Larissa Knapp. “Instead of safeguarding national defense information, the defendant conspired with a foreign national to sell it, potentially endangering our national security.”

The arrest of Sergeant Schultz comes just days after a retired Army lieutenant colonel was charged with sending Ukraine war secrets to a ‘woman’ he met with on a foreign dating site, in what appears to have been a classic honeypot intelligence ploy.

US Air Force employee indicted for leaking secrets on dating app

The 63-year-old retired Army lieutenant colonel is accused of transmitting confidential information to a person claiming to be a woman living in Ukraine

Detailshttps://t.co/9dE5LRosXz pic.twitter.com/n9xNa1pJYX

— RT (@RT_com) March 6, 2024

Tyler Durden

Sat, 03/09/2024 – 18:05

https://www.zerohedge.com/military/army-intel-soldier-charged-selling-secrets-about-us-weapons-ops

“We Will Have A Hard Landing At Some Point. I Guarantee You That…”

“We Will Have A Hard Landing At Some Point. I Guarantee You That…”

Authored by Michael Snyder via The Economic Collapse blog,

Can you guess who the quote in the article title is from? I will give you a hint. It wasn’t me. I know that it sounds like it could have come from me, but it actually comes from a very big name on Wall Street.

Ellen Zentner is Morgan Stanley’s chief U.S. economist, and she is the one that said it.

During an interview with CNBC she warned that “the tightening impacts from monetary policy” will have enormous consequences for the U.S. economy in the months ahead…

“We will have a hard landing at some point. I guarantee you that. We’re all wondering: When does that come?” she said.

“The point that Dimon makes is that there are these cumulative impacts that build over time, and we are in the camp that we haven’t yet seen all of the tightening impacts from monetary policy,” she added, referring to the impact of Fed rate hikes.

She makes a really great point.

{kind=link}

The consequences of interest rate hikes are felt over time.

Higher interest rates have certainly started to cause a lot of problems, but if rates are not brought down soon the level of pain that we are experiencing will begin to go up dramatically.

Unfortunately, the Fed is not likely to reduce interest rates any time soon because inflation continues to run hotter than expected…

Inflation increased by the largest amount in almost a year, according to the Fed’s preferred measure – confirming expectations interest rates will not be cut until around June.

The so-called core personal consumption expenditures (PCE) index – which excludes volatile food and energy prices – increased 0.4 percent between December and January.

Marko Kolanovic, the chief market strategist for JPMorgan Chase, believes that the U.S. economy could be headed into “something like 1970s stagflation”…

In an analyst note to clients, the bank’s chief market strategist Marko Kolanovic warned that the economy may turn away from a “Goldilocks” scenario – in which it is not expanding or contracting by too much – and enter a period of stagflation similar to that experienced in the 1970s.

“Going back to the question of market macro regime, we believe that there is a risk of the narrative turning back from Goldilocks towards something like 1970s stagflation, with significant implications for asset allocation,” Kolanovic wrote.

I would argue that we have already been in a period of stagflation.

The economy has certainly been stagnating, and inflation has been unacceptably high.

But now conditions have taken a dramatic turn for the worse in early 2024, and we are seeing some very troubling signs.

For example, I was stunned to learn that a Canadian pension fund has just sold a stake in a Manhattan office tower for just one dollar…

Canadian pension funds have been among the world’s most prolific buyers of real estate, starting a revolution that inspired retirement plans around the globe to emulate them. Now the largest of them is taking steps to limit its exposure to the most-beleaguered property type — office buildings.

Canada Pension Plan Investment Board has done three deals at discounted prices, selling its interests in a pair of Vancouver towers, a business park in Southern California and a redevelopment project in Manhattan, with the New York stake offloaded for the eyebrow-raising price of just $1. The worry is those deals may set an example for other major investors seeking a way out of the turmoil too.

The Canada Pension Plan Investment Board had a 29 percent stake in Manhattan’s 360 Park Avenue South.

The plan was to redevelop that property, but at this point the outlook for office buildings is so bad that the pension fund just wanted out.

And so the entire 29 percent stake was sold off for just one dollar.

Do you remember when I warned that we were heading into the worst commercial real estate crash in history?

Well, this is what a crash looks like.

Meanwhile, large employers all over America continue to conduct mass layoffs.

Today, I was saddened to learn that Electronic Arts is laying off approximately 700 workers…

Another day, another round of mass layoffs in the games industry. Electronic Arts (EA) has announced it will cut around five percent of its employees, putting almost 700 people out of a job. It’s also cancelling games and shutting down at least one development studio.

EA CEO Andrew Wilson announced the layoffs in an email to employees, which was subsequently posted to the company’s blog on Wednesday.

And we just learned more details about the layoffs that Citigroup is conducting…

Citigroup is cutting nearly 300 workers in New York as it continues its massive layoff spree in an effort to rein in expenses, according to filings with the State Labor Department.

About 239 workers in the primary banking subsidiary, 44 from its broker-dealer unit and three from its technology arm are getting cut, according to Worker Adjustment and Retraining Notification (WARN) notices filed this week.

In early January, the company announced that it was cutting 20,000 roles “over the medium-term,” as part of a reorganization effort. The cuts are slated to save the company between $2 billion and 2.5 billion.

We have not seen anything like this since the Great Recession of 2008 and 2009.

On Thursday, Zero Hedge published a list of 50 different mass layoffs that we have seen recently…

1. Everybuddy: 100% of workforce

2. Wisense: 100% of workforce

3. CodeSee: 100% of workforce

4. Twig: 100% of workforce

5. Twitch: 35% of workforce

6. Roomba: 31% of workforce

7. Bumble: 30% of workforce

8. Farfetch: 25% of workforce

9. Away: 25% of workforce

10. Hasbro: 20% of workforce

11. LA Times: 20% of workforce

12. Wint Wealth: 20% of workforce

13. Finder: 17% of workforce

14. Spotify: 17% of workforce

15. Buzzfeed: 16% of workforce

16. Levi’s: 15% of workforce

17. Xerox: 15% of workforce

18. Qualtrics: 14% of workforce

19. Wayfair: 13% of workforce

20. Duolingo: 10% of workforce

21. Rivian: 10% of workforce

22. Washington Post: 10% of workforce

23. Snap: 10% of workforce

24. eBay: 9% of workforce

25. Sony Interactive: 8% of workforce

26. Expedia: 8% of workforce

27. Business Insider: 8% of workforce

28. Instacart: 7% of workforce

29. Paypal: 7% of workforce

30. Okta: 7% of workforce

31. Charles Schwab: 6% of workforce

32. Docusign: 6% of workforce

33. Riskified: 6% of workforce

34. EA: 5% of workforce

35. Motional: 5% of workforce

36. Mozilla: 5% of workforce

37. Vacasa: 5% of workforce

38. CISCO: 5% of workforce

39. UPS: 2% of workforce

40. Nike: 2% of workforce

41. Blackrock: 3% of workforce

42. Paramount: 3% of workforce

43. Citigroup: 20,000 employees

44. ThyssenKrupp: 5,000 employees

45. Best Buy: 3,500 employees

46. Barry Callebaut: 2,500 employees

47. Outback Steakhouse: 1,000

48. Northrop Grumman: 1,000 employees

49. Pixar: 1,300 employees

50. Perrigo: 500 employees

Just look at that list.

That is nuts!

Anyone that thinks that the U.S. economy is heading in the right direction is simply being delusional.

Greg Hunter just interviewed economic analyst David Morgan, and he is warning that we are actually “entering into a global depression the likes of which the world has never seen”…

Economic analyst and financial writer David Morgan has gone against the majority in the past with predictions that seemed unbelievable at the time. One prediction last year is the Fed not cutting interest rates in 2023. The Fed didn’t, and Morgan is still predicting there will be no Fed interest rate cut anytime soon. Now, with a record high stock market, Morgan is predicting “We are entering into a global depression the likes of which the world has never seen.”

Global central banks were able to delay the inevitable by flooding the system with colossal mountains of money.

But that just created a tremendous amount of inflation and now a horrifying economic crisis is coming anyway.

So I would encourage everyone to brace themselves for the “hard landing” that is rapidly approaching, because it is going to be exceedingly painful for the unprepared.

* * *

Michael’s new book entitled “Chaos” is available in paperback and for the Kindle on Amazon.com, and you can check out his new Substack newsletter right here.

Tyler Durden

Sat, 03/09/2024 – 17:30

https://www.zerohedge.com/economics/we-will-have-hard-landing-some-point-i-guarantee-you

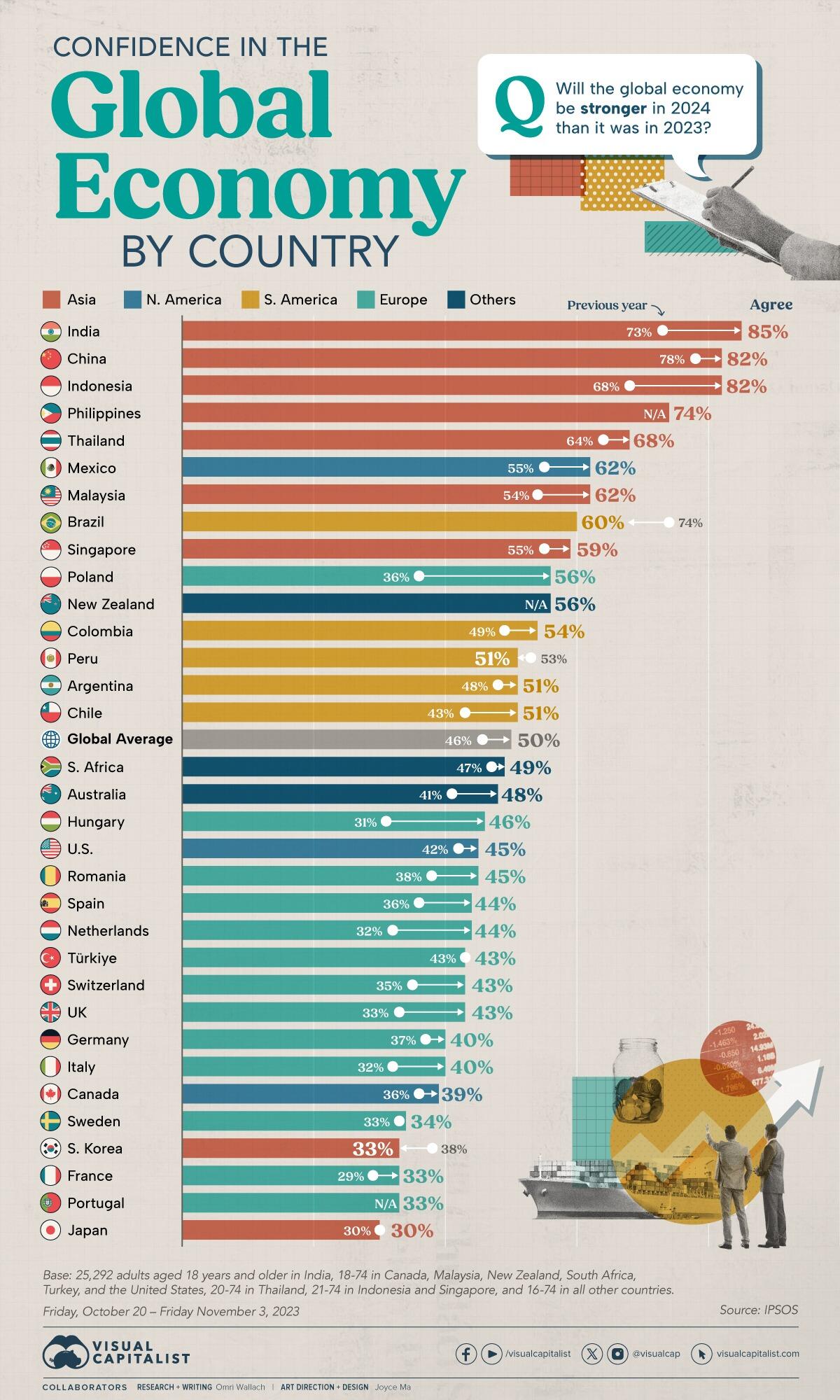

Confidence In The Global Economy, By Country

Confidence In The Global Economy, By Country

Measuring consumer confidence in the economy is crucial for understanding both current economic strength, as well as how consumers may be expected to act in the future.

So how do people around the world feel about the global economy?

This visualization, via Visual Capitalist’s Niccolo Conte, uses survey data collected from October 20 to November 3, 2023 by Ipsos. It was first highlighted as part of our 2024 Global Forecast Series.

{kind=link}

Which Countries Feel Confident About the Economy in 2024?

Heading into 2024, an average of 50% of polled adults felt confident that the global economy would be stronger than in 2023. But breaking down responses by country shows a vast disparity between responses.

Here are the percentage of respondents who agreed with the following statement: “The global economy will be stronger in 2024 than it was in 2023.” We also note the change in percentage points (p.p.) compared with the same question a year prior.

Country

Agree

Change (Year-over-year)

🇮🇳 India

85%

+12 p.p.

🇮🇩 Indonesia

82%

+14 p.p.

🇨🇳 China

82%

+4 p.p.

🇵🇭 Philippines

74%

N/A

🇹🇭 Thailand

68%

+4 p.p.

🇲🇾 Malaysia

62%

+8 p.p.

🇲🇽 Mexico

62%

+6 p.p.

🇧🇷 Brazil

60%

-13 p.p.

🇸🇬 Singapore

59%

+4 p.p.

🇵🇱 Poland

56%

+20 p.p.

🇳🇿 New Zealand

56%

N/A

🇨🇴 Colombia

54%

+5 p.p.

🇨🇱 Chile

51%

+8 p.p.

🇵🇪 Peru

51%

-3 p.p.

🇦🇷 Argentina

51%

+3 p.p.

🇿🇦 South Africa

49%

+2 p.p.

🇦🇺 Australia

48%

+7 p.p.

🇭🇺 Hungary

46%

+15 p.p.

🇷🇴 Romania

45%

+8 p.p.

🇺🇸 United States

45%

+3 p.p.

🇪🇸 Spain

44%

+8 p.p.

🇳🇱 Netherlands

44%

+12 p.p.

🇹🇷 Türkiye

43%

0 p.p.

🇬🇧 Great Britain

43%

+11 p.p.

🇨🇭 Switzerland

43%

+8 p.p.

🇮🇹 Italy

40%

+8 p.p.

🇩🇪 Germany

40%

+3 p.p.

🇨🇦 Canada

39%

+2 p.p.

🇸🇪 Sweden

34%

+1 p.p.

🇫🇷 France

33%

+4 p.p.

🇰🇷 South Korea

33%

-5 p.p.

🇵🇹 Portugal

33%

N/A

🇯🇵 Japan

30%

0 p.p.

🌍 Global average

50%

+4 p.p.

At the top, India, Indonesia, and China stood as being the most confident about 2024’s economic prospects. 85% of Indian respondents agreed that the global economy will be stronger in 2024 than in 2023, while 82% of Chinese and Indonesian respondents felt the same.

Regional disparities also become evident, with Asian countries making up the top five most confident countries and seven out of the top nine. In fact, South Korea and Japan were the only Asian countries surveyed that were not feeling confident, with Japanese respondents being the least confident (30%) and South Koreans tied for the second-least confident (33%).

Countries in South America ranged from Brazil having a high of 60% of respondents agree with 2024 being stronger than 2023 to Chile having a “low” of 51%. North American countries were more split, with Mexico feeling more confident and Canada feeling less confident.

Lastly, Europe stood out as being the least confident in the global economy in 2024. Only Poland (56%) had more than 50% agree that this year would be better than the last, while major economies like Germany (40%) and France (33%) sat closer to the bottom of the table.

Tyler Durden

Sat, 03/09/2024 – 16:55

https://www.zerohedge.com/personal-finance/confidence-global-economy-country

The Coming Of The Police State In America

The Coming Of The Police State In America

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now patrolling the New York City subway system in an attempt to do something about the explosion of crime. As part of this, there are bag checks and new surveillance of all passengers. No legislation, no debate, just an edict from the mayor.

{kind=link}

Many citizens who rely on this system for transportation might welcome this. It’s a city of strict gun control, and no one knows for sure if they have the right to defend themselves. Merchants have been harassed and even arrested for trying to stop looting and pillaging in their own shops.

The message has been sent: Only the police can do this job. Whether they do it or not is another matter.

Things on the subway system have gotten crazy. If you know it well, you can manage to travel safely, but visitors to the city who take the wrong train at the wrong time are taking grave risks.

In actual fact, it’s guaranteed that this will only end in confiscating knives and other things that people carry in order to protect themselves while leaving the actual criminals even more free to prey on citizens.

The law-abiding will suffer and the criminals will grow more numerous. It will not end well.

When you step back from the details, what we have is the dawning of a genuine police state in the United States. It only starts in New York City. Where is the Guard going to be deployed next? Anywhere is possible.

If the crime is bad enough, citizens will welcome it. It must have been this way in most times and places that when the police state arrives, the people cheer.

We will all have our own stories of how this came to be. Some might begin with the passage of the Patriot Act and the establishment of the Department of Homeland Security in 2001. Some will focus on gun control and the taking away of citizens’ rights to defend themselves.

My own version of events is closer in time. It began four years ago this month with lockdowns. That’s what shattered the capacity of civil society to function in the United States. Everything that has happened since follows like one domino tumbling after another.

It goes like this:

1) lockdown,

2) loss of moral compass and spreading of loneliness and nihilism,

3) rioting resulting from citizen frustration, 4) police absent because of ideological hectoring,

5) a rise in uncontrolled immigration/refugees,

6) an epidemic of ill health from substance abuse and otherwise,

7) businesses flee the city

8) cities fall into decay, and that results in

9) more surveillance and police state.

The 10th stage is the sacking of liberty and civilization itself.

It doesn’t fall out this way at every point in history, but this seems like a solid outline of what happened in this case. Four years is a very short period of time to see all of this unfold. But it is a fact that New York City was more-or-less civilized only four years ago. No one could have predicted that it would come to this so quickly.

But once the lockdowns happened, all bets were off. Here we had a policy that most directly trampled on all freedoms that we had taken for granted. Schools, businesses, and churches were slammed shut, with various levels of enforcement. The entire workforce was divided between essential and nonessential, and there was widespread confusion about who precisely was in charge of designating and enforcing this.

It felt like martial law at the time, as if all normal civilian law had been displaced by something else. That something had to do with public health, but there was clearly more going on, because suddenly our social media posts were censored and we were being asked to do things that made no sense, such as mask up for a virus that evaded mask protection and walk in only one direction in grocery aisles.

Vast amounts of the white-collar workforce stayed home—and their kids, too—until it became too much to bear. The city became a ghost town. Most U.S. cities were the same.

As the months of disaster rolled on, the captives were let out of their houses for the summer in order to protest racism but no other reason. As a way of excusing this, the same public health authorities said that racism was a virus as bad as COVID-19, so therefore it was permitted.

The protests had turned to riots in many cities, and the police were being defunded and discouraged to do anything about the problem. Citizens watched in horror as downtowns burned and drug-crazed freaks took over whole sections of cities. It was like every standard of decency had been zapped out of an entire swath of the population.

Meanwhile, large checks were arriving in people’s bank accounts, defying every normal economic expectation. How could people not be working and get their bank accounts more flush with cash than ever? There was a new law that didn’t even require that people pay rent. How weird was that? Even student loans didn’t need to be paid.

By the fall, recess from lockdown was over and everyone was told to go home again. But this time they had a job to do: They were supposed to vote. Not at the polling places, because going there would only spread germs, or so the media said. When the voting results finally came in, it was the absentee ballots that swung the election in favor of the opposition party that actually wanted more lockdowns and eventually pushed vaccine mandates on the whole population.

The new party in control took note of the large population movements out of cities and states that they controlled. This would have a large effect on voting patterns in the future. But they had a plan. They would open the borders to millions of people in the guise of caring for refugees. These new warm bodies would become voters in time and certainly count on the census when it came time to reapportion political power.

Meanwhile, the native population had begun to swim in ill health from substance abuse, widespread depression, and demoralization, plus vaccine injury. This increased dependency on the very institutions that had caused the problem in the first place: the medical/scientific establishment.

The rise of crime drove the small businesses out of the city. They had barely survived the lockdowns, but they certainly could not survive the crime epidemic. This undermined the tax base of the city and allowed the criminals to take further control.

The same cities became sanctuaries for the waves of migrants sacking the country, and partisan mayors actually used tax dollars to house these invaders in high-end hotels in the name of having compassion for the stranger. Citizens were pushed out to make way for rampaging migrant hordes, as incredible as this seems.

But with that, of course, crime rose ever further, inciting citizen anger and providing a pretext to bring in the police state in the form of the National Guard, now tasked with cracking down on crime in the transportation system.

What’s the next step? It’s probably already here: mass surveillance and censorship, plus ever-expanding police power. This will be accompanied by further population movements, as those with the means to do so flee the city and even the country and leave it for everyone else to suffer.

As I tell the story, all of this seems inevitable. It is not. It could have been stopped at any point. A wise and prudent political leadership could have admitted the error from the beginning and called on the country to rediscover freedom, decency, and the difference between right and wrong. But ego and pride stopped that from happening, and we are left with the consequences.

The government grows ever bigger and civil society ever less capable of managing itself in large urban centers. Disaster is unfolding in real time, mitigated only by a rising stock market and a financial system that has yet to fall apart completely.

Are we at the middle stages of total collapse, or at the point where the population and people in leadership positions wise up and decide to put an end to the downward slide? It’s hard to know. But this much we do know: There is a growing pocket of resistance out there that is fed up and refuses to sit by and watch this great country be sacked and taken over by everything it was set up to prevent.

Tyler Durden

Sat, 03/09/2024 – 16:20

https://www.zerohedge.com/political/coming-police-state-america

How Long Do Muslims Fast For Ramadan Around The World?

How Long Do Muslims Fast For Ramadan Around The World?

Ramadan starts on Sunday evening, with the first day of fasting on Monday, March 11 this year. The holy month is based on the Islamic lunar calendar which is 11 days shorter than the Gregorian solar year, and so its start shifts earlier each year.

As Statista’s Anna Fleck details below, while the number of days of Ramadan are equal for all Muslims observing it around the world, the length of the daily fast is not.

During Ramadan, observers vow to abstain from eating, drinking, smoking and sexual activities through daylight hours.

This means that those living further north have to fast for much longer than their counterparts living closer to the equator or even to those in the Southern hemisphere, which is currently tilted away from the sun.

This chart, based on data from website islamicfinder.com, shows how Muslims fasting for Ramadan in Oslo theoretically will have to do so for 15 hours and 15 minutes, while those living in Jakarta, Indonesia, will only need to fast for approximately 13 hours and 13 minutes.

Meanwhile, those living in Melbourne will have just 13 hours and 25 minutes of daylight, depending on the exact day of the Ramadan month.

With the dates of Ramadan moving, there can be a significant difference in the length of fasting depending on the year.

You will find more infographics at Statista

For example, in 2013, Ramadan took place during the peak of summer for the Northern Hemisphere, with countries such as Norway experiencing sundown for only around three hours at night.

This meant practicing communities faced fasts lasting upwards of 20 hours.

To counterbalance this, Muslims may also observe Ramadan using the timetable of Mecca (13 hours and 30 minutes in 2024) or their nearest Muslim city.

Tyler Durden

Sat, 03/09/2024 – 15:45

https://www.zerohedge.com/geopolitical/how-long-do-muslims-fast-ramadan-around-world

Judge Blocks Biden Administration From Illegally Diverting Border-Wall Funds

Judge Blocks Biden Administration From Illegally Diverting Border-Wall Funds

Authored by Caden Pearsen via The Epoch Times,

A federal judge on Friday blocked the Biden administration from unlawfully redirecting taxpayer funds away from the construction of a wall along the southern border.

{kind=link}

Southern District of Texas District Court Judge Drew B. Tipton granted a preliminary injunction after Texas and Missouri sued to stop the scheme, which included diverting the money to other projects like environmental remediation.

“Whether the Executive Branch must adhere to federal laws is not, as a general matter, an area traditionally left to its discretion,” Judge Tipton wrote in his order. The executive branch includes the Department of Homeland Security (DHS).

Judge Tipton, an appointee of President Donald Trump, ruled in favor of the Republican-led states, saying in his ruling that Congress should decide how money is spent, per the U.S. Constitution, and that the Biden administration is not immune from following the law.

President Trump declared a national emergency in February 2019 and used funds from the Departments of Defense and Treasury to construct barriers at the southern border. Congress allocated $1.4 billion explicitly for border wall construction during the 2020 fiscal year to stem the flow of illegal immigration.

However, President Joe Biden, a Democrat, issued an executive order immediately upon taking office in January 2021, terminating the emergency and halting construction. He later directed the DHS to divert the funds to ancillary projects along the border, but not the wall.

This led to both Texas and Missouri filing separate lawsuits against the DHS, which were ultimately combined.

The Biden administration argued that, despite certain language in the law, the DHS should be allowed to spend the money at its discretion.

However, the judge disagreed with this argument, effectively finding that President Biden was wrong to spend funds specifically meant for wall construction on “remediation projects.”

The judge ruled that just because the DHS claimed to have the authority to make certain spending decisions, it doesn’t mean it is free to do whatever it wants.

“Agencies, when afforded congressionally appropriated funds, may expend them only for the proper purpose and amount, and within the authorized period of time,” Judge Tipton wrote.

Therefore, without that discretion, the DHS’s spending decisions “run afoul” of the law, specifically violating the Administrative Procedure Act (APA).

Judge Tipton wrote in his order that the way Congress wrote the law was quite specific in saying the money should go to barriers along the border.

“The central question in this case, then, is this: Has the Government obligated FY 2020 and FY 2021 funds for the ‘construction of [a] barrier system’? The answer is largely no,” the judge wrote.

The Biden administration’s new border plan, unveiled by the Department of Defense and the DHS in June 2021 and updated about a year later, contemplated spending the funds on flood control, cleanup, and environmental remediation projects. This would include adding lighting, cameras, and detection technology at locations where a physical barrier had already been constructed.

Under the plan, most border wall projects were canceled, and all the existing barrier infrastructure previously funded by the DOD was transferred to the DHS’s control.

The attorneys general of Texas and Missouri, who challenged these spending decisions, hailed the ruling on Friday.

“Today, I secured a preliminary injunction against an attempt by the Biden Administration to illegally redirect statutorily obligated funds away from the construction of a border wall,” Texas Attorney General Ken Paxton said in a statement.

“Biden acted completely improperly by refusing to spend the money that Congress appropriated for border wall construction, and even attempting to redirect those funds,” he continued. “His actions demonstrate his desperation for open borders at any cost, but Texas has prevailed.”

Missouri Attorney General Andrew Bailey called the ruling a “huge step” in fighting to secure the southern border.

“The Biden Administration has failed to abide by the law to finish the construction of a wall along the southwest border,” Mr. Bailey said in a statement. “Joe Biden refuses to carry out his constitutionally mandated responsibilities, so we took him to court to force him to do his job. This is a huge step forward in the fight to secure our border at a key moment in our nation’s history.”

Tyler Durden

Sat, 03/09/2024 – 15:10

Denver Asks Landlords To Rent To Illegals

Denver Asks Landlords To Rent To Illegals

The city of Denver, Colorado has asked landords to start renting to illegal immigrants, Denverite reports.

{kind=link}

On Tuesday, the city launched a program gathering information from landlords with property vacancies that rent for less than $2,000 per month. The city’s goal is to connect property owners with new immigrants in need of permanent housing.

Jon Ewing, spokesperson for Denver Human Services, said the city has already started hearing from landlords who want to work with the city on the effort.

The program was launched as the city continues to close temporary hotel shelters in an effort to scale back costs, which Mayor Mike Johnston announced at the end of February – a move he said could save the city some $60 million out of an anticipated $180 million in expenses related to the migrants.

According to city data, the number of people being housed in the shelters has dropped from 5,200 in mid-January to 2,000 at present.

“For ongoing housing, we’re trying to do more and better at the case navigation that gets people directly from shelter opportunities into housing, or into workforce options for normal travel, and so that continues to be our focus and it’s been successful for us over the last five weeks,” Johnson said at a press conference last week.

The migrants, mostly from Venezuela, have been looking for long-term housing in an increasingly unaffordable housing market. Complicating matters, many new immigrants lack work authorization that would allow them to secure legal employment in order to prove their income.

“We definitely need assistance in finding out what else is out there,” said Yoli Cassas, executive director of nonprofit ViVe Wellness, who says she opes that the city’s call to landlords will help open other housing resources that are currently unavailable.

“It’s been great because that means we’re gonna get more inventory to work with, which is what’s needed,” Casas said.

Tyler Durden

Sat, 03/09/2024 – 14:35

https://www.zerohedge.com/political/denver-asks-landlords-rent-illegals